For the 30th year in a row, the mild-mannered Labrador retriever is the most popular dog in the U.S. A great choice as a pet, this breed is credited for being exceptionally affectionate and good around children as well as other dogs. But no matter what variety your pet may be, even the best dog affects homeowners insurance.

Dog ownership and insurance can be an emotionally charged topic because, let’s face it, talking about our pets is like discussing a loved one. With that said, keep an open mind and objective eye when considering how dog ownership affects your homeowners insurance coverage.

Hidden Value

We often think of homeowners insurance as only protecting the home. However, one of its most valuable coverages is the personal liability protection it provides. Courts hold owners liable for injury and damage caused by their pets, and the personal liability protection on a homeowners insurance policy can guard against such an event.

Dog Facts and Statistics

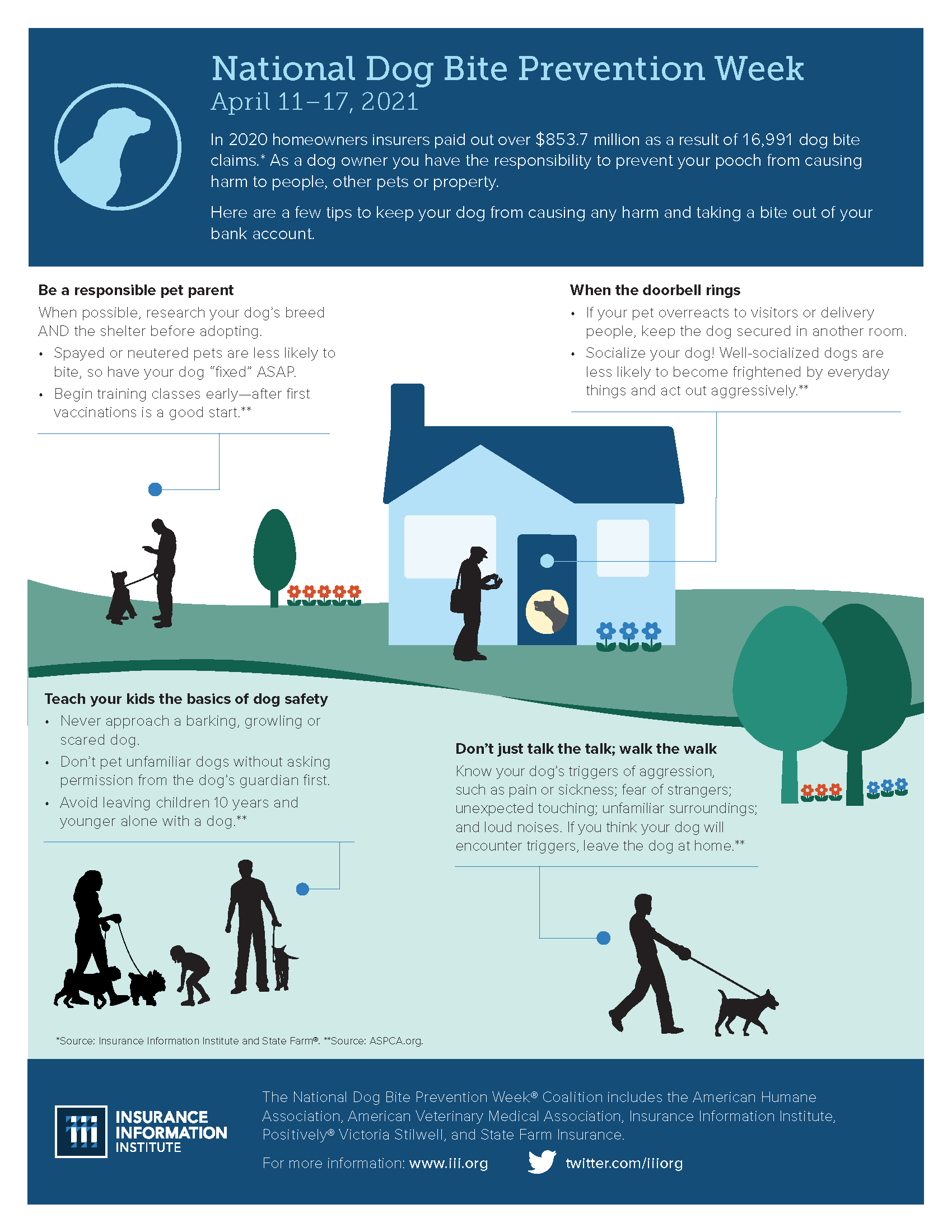

The Insurance Information Institute reports that 69% of all households in the U.S. have a dog. In 2020, insurance companies paid over $853,700,000 from 16,991 dog bite claims. That is an average of over $50,000 per dog bite. When we consider those facts from the insurance company’s perspective, we see that over 69% percent of homes they insure have the potential at any time to have a $50,000 claim solely due to the family pet. Thus, it is understandable that they pay particular attention to our pets, ask probing questions when applying for insurance, and take steps to limit this liability.

“But my dog has never bitten anyone.” We hear this from many clients and, to be fair, you’re probably right. However, insurance is concerned with future risk, and there is no such thing as a dog that cannot bite. Further, bite claims are only a portion of the risk raised by dogs.

Dog Liability

Insurance companies have found that a dog with a bite history will likely bite again, no matter what controls a homeowner may put in place. This is why homeowners with dogs that have bitten will pay more for their coverage. But bites are not the only way dogs can cause injury. Even the most docile pets have caused large claims by knocking down children or elderly, running into bicyclists, and causing traffic accidents.

More on dog bite liability.

Fortunately, most dog bites are preventable. Here are a few tips if you have a dog at home.

More Info

- Get them around people early and often. Start when they’re a puppy and make their socialization a priority. The more often they interact with people at a young age, the better they will respond calmly in an uncertain situation.

- Train yourself to train your dog. Understand how it thinks. Dogs are pack animals and think completely differently than we do. Speak with a trainer. Read a book. Attending obedience classes is one of the best investments you can make.

- Be conscientious of roughhousing. If children are playing with the dog, be sure the fun is non-aggressive. It’s better to play fetch than tug of war.

- Overstimulation often leads to dog bites. Give your dog a chance to rest away from people and kids. Steer clear of stressful situations.

Dog Damage

Though less frequent, dogs are known to cause damage to property of others. Insurance companies see claims for dogs breaking through fences, digging up flower beds, chewing through wires and cabling, chewing through house siding, killing grass by urination, hurting other dogs, and hurting other cats or pets. Because this damage is done to someone else or their property, personal liability from the homeowners policy should provide protection.

However, if an owner’s dog chews through their own home’s drywall or breaks through a fence, such repairs will not be covered. Notice the difference: if the animal hurts someone else or damages someone else’s property, that is covered. But if they injure one of their home’s occupants or damage their home, that is not covered.

Affects Upon Insurance Policies

Because of the increased potential for claims, some insurance companies charge more for insuring homes that have dogs than those that do not. Another common tactic is to decline to quote coverage for homeowners that own certain dog breeds that have higher rates of biting. Lastly, some offer homeowners coverage but exclude liability associated with dogs. One such example is a policy that excludes liability coverage for issues, “Caused by or originating from any canine, hybrid canine…”

Breeds that may cause insurance companies to raise questions are pit bull, rottweiler, German shepherd, Doberman pinscher, chow chow, wolf and wolf hybrids, akita, husky, mastiff, and a few others. Notice that most of these animals are larger breeds. This is because, even though some small breeds bite more often, damage is less likely and they usually do not result in a claim.

“But dog claims are usually the fault of bad owners, and I’m a good owner.” It is true that many dog claims are due to dog owners being poor pet parents. However, insurance companies have no way to determine whether someone properly trains, exercises, and disciplines their dog. Thus, they must look to other means to manage the risk.

Talk To Your Insurance Agent

The best way to reduce the risk of a dog bite is to be a thoughtful and informed owner. Next, review your home insurance policy. If you have any questions regarding coverage, contact our insurance agent. We will help determine your risks and advise how to cover them. Not a client of ours? Let us earn your business! Each of our clients is assigned a personal insurance agent and provided their email address as well as a phone number that rings right on their desk.

Was this post helpful?

- Share it using the links below

- Review all our personal insurance posts

- Review all our personal insurance products

- Subscribe

Comments are closed.